Overview

As of November 23, 2018, the Internal Revenue Service (“IRS”) published proposed regulations providing some valuable guidance with respect to the upcoming sunset of the increased estate and gift tax exemption in the Tax Cuts and Jobs Act (“TCJA”).1 With the TCJA, the estate tax exemption amount was increased from $5.49 Million to $11.18 Million (after factoring the inflation adjustments), but only temporarily. After 2025, the exemption goes back to pre-TCJA amounts, albeit indexed for inflation. For anyone who is familiar with the actual computation of the estate tax of a decedent potentially having a taxable estate and having made gifts during life, the way the calculation works did not exactly work with a temporary increase due to the potential for a “clawback.” Some commentators thought it was “use it or lose it.” Others felt that this only worked if one died before the sunset.

Calculation of the Gift and Estate Taxes

The calculation of the estate tax is a bit odd. On its face, you have an exemption, make lifetime gifts, and eventually die having assets included in your taxable estate. But wait, there is a unified credit, numbers are run against the rate tables, tentative tax is calculated, and the tentative tax is then reduced by the unified credit resulting in the net estate tax owed. There are actually quite a few steps along the way. But, the nagging issue of this method (and the way tax is calculated on estate and gift tax returns, Forms 706 and 709), is that we start over on the calculations each time. In essence, the calculation is performed cumulatively in nature. The actual steps to determine gift tax imposed under IRC 2501 and estate tax under IRC 2001(a) are as follows:

Gift Tax Computation Steps

- Determine the tentative tax (tax unreduced by the credit amount) on the sum of all taxable gifts);

- Determine the tentative tax on the taxable gifts made in all prior periods;

- Determine net tentative gift tax for current year [(2) – (1)];

- Determine credit equal to the applicable credit amount;2

- Determine the sum of the amounts allowable as credit to offset the gift tax on gifts made by donor in all preceding calendar years;3

- Determine remaining credit amount. [(4) – (5)]; and4

- Determine gift tax [(3)-(6)].

Computation as Shown on Form 7095

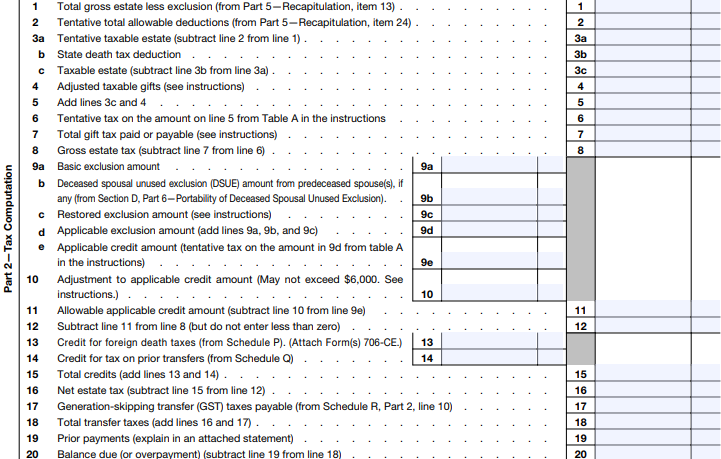

Estate Tax Computation Steps

- Determine the tentative tax (tax unreduced by the credit amount) on the sum of the taxable estate and adjusted taxable gifts, defined as all taxable gifts made after 1976 other than those included in the gross estate);

- Determine hypothetical gift tax (a gift tax reduced, but not to below zero, by the credit amounts allowable in the years of the gifts) on all post-1976 taxable gifts, whether or not included in the gross estate. This hypothetical gift tax is referred to as the gift tax payable;6

- Determine net tentative gift tax payable for current year [(2) – (1)];

- Determine credit equal to the applicable credit amount. Such credit may not exceed the net tentative estate tax;7 and

- Determine estate tax. [(3) – (4)].8

Computation as Shown on Form 7069

Resolution through Proposed Regulations

Under Prop. Reg. 20.2010-1, which is set to modify the current Treas. Reg. 20.2010-1, subsection (c) , decedents’ estates will be able to add back that portion of credit used that was utilized during a period where the exemption was higher, but only to the extent such credit used was utilized beyond the current exemption amount. In short, the Treasury says “Use it, or lose it!”

See the example scenario below:

| Assume Gifts made in 2018 | |||

| Sample Scenario | Enhanced Period | w/o Prop Reg | w/ Prop. Reg. |

| 2018 | 2026 | 2026 | |

| Gross Exemption | 11,180,000 | 6,500,000 | 6,500,000 |

| Prior Exemption Used | 1,000,000 | 9,500,000 | 9,500,000 |

| Remaining Exemption | 10,180,000 | – | – |

| Preserved Used Excess Exemption | – | – | 3,000,000 |

| Adjusted Gross Exemption | 11,180,000 | 6,500,000 | 9,500,000 |

| Assumptions | |||

| Starting Assets | 25,000,000 | 20,000,000 | 20,000,000 |

| Current Gifts/Estate | 8,500,000 | 20,000,000 | 20,000,000 |

| Prior Gifts | 1,000,000 | 9,500,000 | 9,500,000 |

| Simplified Calculations | |||

| Total Gifts/Estate | 9,500,000 | 29,500,000 | 29,500,000 |

| Less: Exemption | (11,180,000) | (6,500,000) | (9,500,000) |

| Gifts in Excess of Exemption | – | 23,000,000 | 20,000,000 |

| Remaining Exemption | 1,680,000 | – | – |

| Tax Owed | – | 9,200,000 | 8,000,000 |

| Savings | 1,200,000 | ||

How to Make the Most of the TCJA Exemption

Right now, we still have several years to go before the sunset arrives. However, it is likely advisable for most people who may have a taxable estate to consider making gifts prior to sunset (2026) to ensure utilization of the enhanced exemption amounts under the TCJA. Each person’s situation will differ, and a careful analysis of income tax cost basis step-up potential, personal financial impact, and the individual tax situation for each person will be crucial in determining the best approach.

Footnotes

- 83 FR 59343 (Text of Proposed Regulations)

- The applicable credit amount is the tentative tax on the applicable exclusion amount as if the donor died on the last day of the current calendar year. The applicable exclusion amount is the sum of the basic exclusion amount in effect for the year in which the gift was made, plus any deceased spouse unused exclusion amount as of the date of the gift, and any restored exclusion amount as of the date the gift per Notice 2017-15.

- For the purposes of this determination, the allowable credit for each preceding calendar period is the tentative tax, computed at the tax rates in effect for the current period, on the applicable exclusion amount for such prior period, but not exceeding the tentative tax on the gifts actually made during such prior period.

- See IRC §§ 2502, 2505

- From 2017 Form 709

- The credit amount allowable for each year during which a gift was made is the tentative tax, computed using the tax rates in effect at the decedent’s death, on the applicable exclusion amount for that year, but not exceeding the tentative tax on the gifts made during that year. Section 2505(c). The applicable exclusion amount is the sum of the basic exclusion amount as in effect for the year in which the gift was made, any deceased spouse unused exclusion amount as of the date of the gift, and any restored exclusion amount as of the date of the gift per Notice 2017-15.

- The applicable credit amount is the tentative tax on the applicable exclusion amount as if the donor died on the last day of the current calendar year. The applicable exclusion amount is the sum of the basic exclusion amount in effect for the year in which the gift was made, plus any deceased spouse unused exclusion amount as of the date of the gift, and any restored exclusion amount as of the date the gift per Notice 2017-15.

- See IRC §§ 2502, 2505

- From 2017 Form 706.